Georgi Stankov, April 16, 2016

There is a new significant development regarding the official acknowledgement that the eight biggest banks in the USA, which are dubbed as “too-big-to-fail” due to their catastrophic spill-over effect on the entire financial system are illiquid and de facto bankrupt. This explains the three emergency meetings this week in the Fed and then the Fed chairman Yellen with Bombama and his grey Reptilian eminence, VP Biden, as reported by myself.

Read: The 12th Hour

As the Wall Street Journal reports two Federal regulators, the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC), are set to “reject” the living wills of potentially four systemically important banks, including the largest bank in the U.S., JPMorgan Chase. The three other banks named are Bank of New York Mellon, State Street and Bank of America, all of them building the core of the Orion banking system of Rockefeller and Rothschild. Please observe that these banks also possess the Fed.

Under Section 165 of the financial reform legislation known as Dodd-Frank, banks designated as systemically important must submit living wills to the Fed and FDIC explaining how they can be “rapidly” liquidated if they fail without bringing down the rest of the financial system – as occurred in 2008. This is the latest development of a systemic fraud that was revealed at one instant in the Senate but then again sent into oblivion until the inevitable comes these days.

On July 15, 2014 during a Senate Banking hearing between Senator Elizabeth Warren and Fed Chair Janet Yellen on the matter of these living wills. Warren told Yellen that at the time of its collapse in 2008, Lehman Brothers had $639 billion in assets and 209 subsidiaries and it took three years to unwind the bank in bankruptcy. Warren singled out JPMorgan Chase for comparison, saying that it has $2.5 trillion in assets and 3,391 subsidiaries.

Dodd-Frank specifically states that these wind-down plans must be “credible” each year or the Fed and FDIC must reject them and force the banks to take remedial steps such as simplifying their structure or selling off assets.

Yellen was clearly not prepared for this line of questioning and stumbled badly in her answers to Warren. She said the Fed was pursuing a “process,” that the plans are “complex” with some banks submitting plans that are “tens of thousands of pages.” Yellen then summed up with this:

“I think what was intended is this interpretation you’re talking about, whether they’re credible, in other words, do they facilitate an orderly resolution, and I think we need to give these firms feedback.”

This hearing came more than six years after the greatest Wall Street banking collapse since the Great Depression and Warren was visibly agitated by these stonewalling answers from Yellen. Warren responded:

“I have to say, Chair Yellen, I think the language in the statute is pretty clear, that you are required, the Fed is required, to call it every year on whether these institutions have a credible plan — and I remind you, there are very effective tools that you have available to you that you can use if those plans are not credible, including forcing these financial institutions to simplify their structure or forcing them to liquidate some of their assets — in other words, break them up.

And I just want to say one more thing about this process, the plans are designed not just to be reviewed by the Fed and the FDIC, but also to bring some kind of confidence to the marketplace and to the American taxpayer that in fact there really is a plan for doing something if one of these banks starts to implode.”

The truth is that there is no such plan and the public has never been allowed to see those 10,000 pages of what it would take to unwind one of the banking behemoths. Warren’s reference to bringing “confidence to the marketplace” was called into further question on Tuesday when the Government Accountability Office (GAO) released its own study on the living wills, which they refer to as “Resolution Plans.”

The GAO noted that the FDIC’s Board of Directors determined that all of the 2013 plans submitted by systemically important banks with more than $250 billion in non-bank assets were “not credible” or “would not facilitate an orderly resolution under the Code.” The Federal Reserve, however, made no such determination and simply said the banks would have to improve their plans going forward. This response is no surprise, after all these banks possess the Fed. How can the Fed exert any control over these banks. It is as if to “make the bock the gardener” to quote a German saying (Den Bock zum Gaertner machen). This is the kind of lunacy we are dealing with in this last phase of the Ascension scenario.

The GAO also gave low marks to the regulators in terms of public transparency on the living will process, writing in the report that:

“FDIC and the Federal Reserve are considering publicly providing more information about their resolution plan reviews. Federal Reserve officials told us that while they were continuously evaluating the release of more plan information into the public domain, they did not have a time frame for reaching a decision on this issue. FDIC officials also told us that the regulator was considering disclosing more information about its review process but had not yet reached the point of sharing such information with the public.”

This is the usual smoke and mirrors tactic the banksters always employ when they want to hide their weak cards. However, one stark analysis provided in the GAO report focused on Lehman Brothers’ difficulties in unwinding itself. Two key points mentioned were that:

“Lines of business were fragmented across numerous subsidiaries on three different continents. “The filing created an ‘event of default’ for its derivatives, resulting in the termination of more than 900,000 contracts.”

According to its website, JPMorgan Chase does business in 60 countries, 20 times the number as Lehman. And while Lehman Brothers had $35 trillion in notional derivatives at the time of its failure, JPMorgan Chase had $51 trillion as of December 2015 according to data released by the Office of the Comptroller of the Currency.

Then there is the question as to whether JPMorgan Chase has actually simplified its operations or is simply reporting less to the public and its regulators. According to the list of “significant legal entity subsidiaries” as of December 31, 2015 that it filed with the Securities and Exchange Commission, it has a mere 42 companies. That’s a far cry from the 9 pages of subsidiaries it filed with the SEC as recently as December 31, 2013 and the statement from Senator Warren in July 2014 that JPMorgan Chase had 3,391 subsidiaries. Here we have the usual accounting gimmicks of a Ponzi scheme that has penetrated like a cancer the global financial system. For further information on the impending bankruptcy of JPMorgan Chase see also the interview with Reggie Middleton here.

One can find a similar fraudulent pattern at Citigroup when one looks at the subsidiaries it’s now reporting versus major companies it still owns but that have disappeared in its filings. After all we are talking about the US of Accounting Gimmicks.

In addition to the living wills, the Fed is also supposed to be overseeing stress tests at the systemically important banks to make sure they could survive a serious economic downturn. But as recently as last month, researchers at the U.S. Treasury’s Office of Financial Research (OFR) found that the Fed was going about that all wrong, writing that the Fed is measuring counter-party risk on a bank by bank basis while the real risk is what would happen if a large counter-party to multiple systemically important banks failed.

According to the OFR study, just six banks make up the “core” of the U.S. financial system. That is six banks out of a total of 6,172 commercial banks in the U.S. Those banks are: Bank of America Corp., Citigroup Inc., Goldman Sachs Group, Inc., JPMorgan Chase Co., Morgan Stanley, and Wells Fargo & Co.

The researchers found that while individual bank holding company’s direct losses have declined under the Fed’s stress tests, “counter-party credit risks to the banking system collectively have risen and may suggest a greater systemic risk than is commonly understood.” It has been a key argument in all my financial articles that there is a systemic risk in this financial Ponzi scheme as all big banks are hugely exposed to mutual derivative contracts of more than $900 trillion in total (20 times the world GDP) so that it is sufficient for one bank to declare bankruptcy and the entire banking system will immediately collapse. This is what I defined as Financial Apoptosis – sudden death of the banking system – that can happen any moment. The parents now devour their children as the Olympic Gods in the gruesome Greek mythology. Another analogy – the sudden death of the banks will be like chain reaction leading to a sudden nuclear implosion of the entire financial system.

As the financial source Wall Street on Parade writes on this issue, the key question is now:

“If the Wall Street Journal is correct and the Fed and FDIC have finally rejected JPMorgan’s tricked up version of global banking reality, the real question will be what happens next. Will the regulators come clean with the public as to why JPMorgan’s plan is not credible or will they continue to hide behind the veil of supervisory confidentiality. Will they force JPMorgan to shrink its global footprint and get out of high risk gambling ventures like that of the London Whale episode. Will the regulators ask JPMorgan to get back to the business of banking and exit commercial businesses and physical commodities where the public never intended banks to operate.”

It is obvious that these are the most clear signs we have seen so far that the collapse of the Orion financial system is impending and the payday for the sins of the banksters is very close – it is also the day of our ascension. Here is another reason why:

_____________________________

The Fed Sends a Frightening Letter to JPMorgan and Corporate Media Yawns

By Pam Martens and Russ Martens: April 14, 2016

Yesterday the Federal Reserve released a 19-page letter that it and the FDIC had issued to Jamie Dimon, the Chairman and CEO of JPMorgan Chase, on April 12 as a result of its failure to present a credible plan for winding itself down if the bank failed. The letter carried frightening passages and large blocks of redacted material in critical areas, instilling in any careful reader a sense of panic about the U.S. financial system.

A rational observer of Wall Street’s serial hubris might have expected some key segments of this letter to make it into the business press. A mere eight years ago the United States experienced a complete meltdown of its financial system, leading to the worst economic collapse since the Great Depression. President Obama and regulators have been assuring us over these intervening eight years that things are under control as a result of the Dodd-Frank financial reform legislation. But according to the letter the Fed and FDIC issued on April 12 to JPMorgan Chase, the country’s largest bank with over $2 trillion in assets and $51 trillion in notional amounts of derivatives, things are decidedly not under control.

At the top of page 11, the Federal regulators reveal that they have “identified a deficiency” in JPMorgan’s wind-down plan which, if not properly addressed, could “pose serious adverse effects to the financial stability of the United States.” Why didn’t JPMorgan’s Board of Directors or its legions of lawyers catch this?

It’s important to parse the phrasing of that sentence. The Federal regulators didn’t say JPMorgan could pose a threat to its shareholders or Wall Street or the markets. It said the potential threat was to “the financial stability of the United States.”

That statement should strike fear into even the likes of presidential candidate Hillary Clinton who has been tilting at the shadows in shadow banks while buying into the Paul Krugman nonsense that “Dodd-Frank Financial Reform Is Working” when it comes to the behemoth banks on Wall Street.

How could one bank, even one as big and global as JPMorgan Chase, bring down the whole financial stability of the United States?

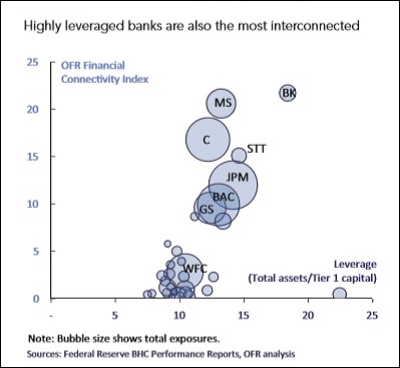

Because, as the U.S. Treasury’s Office of Financial Research (OFR) has explained in detail and plotted in pictures (see below), five big banks in the U.S. have high contagion risk to each other. Which bank poses the highest contagion risk? JPMorgan Chase.

The OFR study was authored by Meraj Allahrakha, Paul Glasserman, and H. Peyton Young, who found the following:

“…the default of a bank with a higher connectivity index would have a greater impact on the rest of the banking system because its shortfall would spill over onto other financial institutions, creating a cascade that could lead to further defaults. High leverage, measured as the ratio of total assets to Tier 1 capital, tends to be associated with high financial connectivity and many of the largest institutions are high on both dimensions… The larger the bank, the greater the potential spillover if it defaults; the higher its leverage, the more prone it is to default under stress; and the greater its connectivity index, the greater is the share of the default that cascades onto the banking system. The product of these three factors provides an overall measure of the contagion risk that the bank poses for the financial system.”

The Federal Reserve and FDIC are clearly fingering their worry beads over the issue of “liquidity” in the next Wall Street crisis. That obviously has something to do with the fact that the Fed has received scathing rebuke from the public for secretly funneling over $13 trillion in cumulative, below-market-rate loans, often at one-half percent or less, to the big U.S. and foreign banks during the 2007-2010 crisis (see also here, note George). The two regulators released background documents yesterday as part of flunking the wind-down plans (living wills) of five major Wall Street banks. (In addition to JPMorgan Chase, plans were rejected at Wells Fargo, Bank of America, State Street and Bank of New York Mellon.) One paragraph in the Resolution Plan Assessment Framework and Firm Determinations (2016) used the word “liquidity” 11 times ( I am saying since 2008 that all big Orion banks have no liquidity as their leverage is more than 50: 1 high and any serious contraction of the real economy as we observe currently will lead to massive bad loans and will crash the fragile financial structure of these banks which is merely a Potemkin facade hiding innumerous debt gaps. Note, George):

“Firms must be able to reliably estimate and meet their liquidity needs prior to, and in, resolution. In this regard, firms must be able to track and measure their liquidity sources and uses at all material entities under normal and stressed conditions. They must also conduct liquidity stress tests that appropriately capture the effect of stresses and impediments to the movement of funds. Holding liquidity in a manner that allows the firm to quickly respond to demands from stakeholders and counter-parties, including regulatory authorities in other jurisdictions and financial market utilities, is critical to the execution of the plan. Maintaining sufficient and appropriately positioned liquidity also allows the subsidiaries to continue to operate while the firm is being resolved. In assessing the firms’ plans with regard to liquidity, the agencies evaluated whether the companies were able to appropriately forecast the size and location of liquidity needed to execute their resolution plans and whether those forecasts were incorporated into the firms’ day-to-day liquidity decision-making processes. The agencies also reviewed the current size and positioning of the firms’ liquidity resources to assess their adequacy relative to the estimated liquidity needed in resolution under the firm’s scenario and strategy. Further, the agencies evaluated whether the firms had linked their process for determining when to file for bankruptcy to the estimate of liquidity needed to execute their preferred resolution strategy.”

Apparently, the Federal regulators believe JPMorgan Chase has a problem with the “location,” “size and positioning” of its liquidity under its current plan (This is a polite circumscription that the bank is bankrupt. Note, George). The April 12 letter to JPMorgan Chase addressed that issue as follows:

“JPMC does not have an appropriate model and process for estimating and maintaining sufficient liquidity at, or readily available to, material entities in resolution…JPMC’s liquidity profile is vulnerable to adverse actions by third parties.”

The regulators expressed the further view that JPMorgan was placing too much “reliance on funds in foreign entities that may be subject to defensive ring-fencing during a time of financial stress.” The use of the term “ring-fencing” suggests that the regulators fear that foreign jurisdictions might lay claim to the liquidity to protect their own financial counter-party interests or investors.

JPMorgan’s sprawling derivatives portfolio that encompasses $51 trillion notional amount as of December 31, 2015 is also causing angst at the Fed and FDIC. The regulators wanted more granular detail on what would happen if JPMorgan’s counter-parties refused to continue doing business with it if rating agencies cut its credit ratings. The regulators asked for a “narrative describing at least one pathway” for winding down the derivatives portfolio, taking into account a number of factors, including “the costs and challenges of obtaining timely consents from counter-parties and potential acquirers (step-in banks).” The regulators wanted to see the “losses and liquidity required to support the active wind-down” of the derivatives portfolio “incorporated into estimates of the firm’s resolution capital and liquidity execution needs.”

According to the Office of the Comptroller of the Currency’s (OCC) derivatives report as of December 31, 2015, JPMorgan Chase is only centrally clearing 37 percent of its derivatives while a whopping 63 percent of its derivatives remain in over-the-counter contracts between itself and unnamed counterparties. The Dodd-Frank reform legislation had promised the public that derivatives would all become exchange traded or centrally cleared. Indeed, on March 7 President Obama falsely stated at a press conference that when it comes to derivatives “you have clearinghouses that account for the vast majority of trades taking place.”

But the OCC has now released four separate reports for each quarter of 2015 showing just the opposite of what the President told the press and the public on March 7. In its most recent report the OCC, the regulator of national banks, states that “In the fourth quarter of 2015, 36.9 percent of the derivatives market was centrally cleared.” (This is another significant proof for the gargantuan fraud of the Bombama government in cahoots with the Wall Street banksters. Note, George)

Equally disturbing, the most dangerous area of derivatives, the credit derivatives that blew up AIG and necessitated a $185 billion taxpayer bailout, remain predominately over the counter. According to the latest OCC report, only 16.8 percent of credit derivatives are being centrally cleared. At JPMorgan Chase, more than 80 percent of its credit derivatives are still over-the-counter. (This key fact explains why the occurrence of the financial apoptosis is unpredictable but unavoidable as nobody has an overview or controls the credit derivatives market. Note, George)

Three of the five largest U.S. banks (JPMorgan Chase, Bank of America and Wells Fargo) have now had their wind-down plans rejected by the Federal agency insuring bank deposits (FDIC) and the Federal agency (Federal Reserve) that secretly sluiced $13 trillion in rollover loans to the insolvent or teetering banks in the last epic crisis that continues to cripple the country’s economic growth prospects. Maybe it’s time for the major newspapers of this country to start accurately reporting on the scale of today’s banking problem (This is the perpetuation of the governmental and banksters’ fraud by the MSM that also belong to the bankster cabal, just as the latter have bought all politicians. Hence the only possible outcome is sudden financial collapse as all these regulatory gimmicks are applied to a house of cards. Note, George).